I really wanted to wait. I wanted to write this blog post after the market closes on Friday (March 12, 2021). MicroVision (the company) and MVIS (its stock) are both moving so quickly that waiting a day can change the story; but in that case, there’s value in telling this story then that story. Today (March 11, 2021), they announced earnings. Tomorrow, the market will officially react. In the last ten years of this blog, I’ve written about them over a hundred times. At some level the story’s stayed the same. There have also been a lot of changes; so, I guess I’ll add today’s activity to the list.

One of the biggest changes has been the attention to stock is getting. The company is getting attention, too; but from what I read in social media and see on YouTube, many people are finding the stock first. Many of the recent discussions call MicroVision an LiDAR company, ignoring the augmented vision work. Or, it’s an augmented reality company; which also seems to have a LiDAR product. Or. Or. MicroVision is many things. They’re working on LiDARs for autonomous vehicles, and LiDAR for the home, and wearable displays, and stand-alone displays, and interactive displays, and in the past worked on bar code scanners, medical equipment, and, and, and … oh, yeah, projectors small enough to embed in smartphones.

MicroVision is basically a company that has many (somewhat aging) patents on all of those things based on an ingenious chip design which incorporates an oscillating mirror. Shine a light on it, and it can paint a picture. Let the world provide the light, and let the outside image hit a sensor. Visible light out becomes a picture. Visible light in becomes a camera. Other parts of the electromagnetic spectrum and get LiDAR. Get fancy and make a display and a sensor, add sophisticated software and create touch-free interactive displays. Cruise the discussion boards and be overwhelmed with creative ideas being played with by enthusiastic shareholders. But, the company has rarely made significant money; yet, is still in business. Great potential. Terrible financials.

A confluence or a collision of events have changed the company’s and the stock’s situation.

Because so many people found the company via the stock, let’s step there, next.

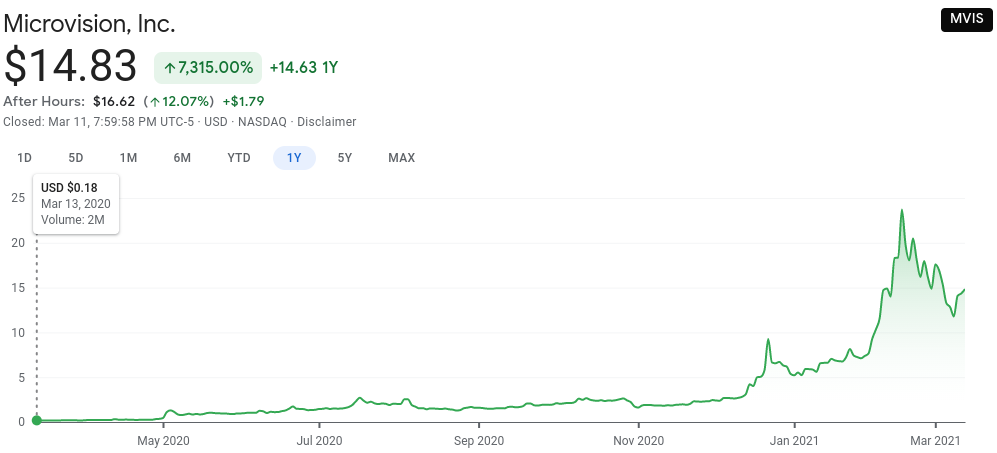

Within the last year, the stock is up 7,315%. That is NOT 7.315%, which would be a typical increase for a market average. Within the last year the stock has gone from under $0.20 to a high of over $24. It is fun realizing someone became a new shareholder about this time last year, held, and has reason to smile even as the stock retreated to under ‘only’ $15.

Many people are crediting the current CEO for everything. I suspect over twenty years of efforts led to that day last year, and to today.

The biggest news has been LiDAR. LiDAR is basically radar but using a different part of the spectrum. LiDAR and radar are powerful tools, but fitting them into a car at a reasonable price has been difficult. Early prototypes used something that supposedly cost about $10,000 per unit and was the size of a KFC bucket. Not elegant, but successful enough to further the technology. I don’t know the exact dimensions, but MicroVision’s version looks to be about the size of a carton of eggs, supposedly will cost about $1,000, and may have performance superior to the competition. Maybe. The units aren’t in mass-production, haven’t been certified by the customers or the regulatory agencies, and are like any new technology – needing to prove themselves. But. It sounds like the customers like the MicroVision units. Production-quality units are intended to be shipped out in April. (Check the company web site for details.)

The second most notable news has been the augmented reality components. Microsoft is using MicroVision components in their Hololens product. That went a bit quiet about the time that Covid hit; but Microsoft continues to develop and expand the product. But when will the revenues arrive, and will Microsoft’s experience inspire more customers?

Then, there’s the possible display customers, the interactive display customers, the consumer version of LiDAR for things like in-home security, and … I’m undoubtedly missing something.

MicroVision is more than any one of those product lines.

Oh yes, and the company was in such a sad situation within the last year that the CEO became much more active in trying to find a buyer.

Take your pick. Which one of those is what started and fueled a 7,000% increase in the stock price – even as the revenues remain almost inconsequential? Many are pointing at their favorite. Add them up. Scroll through Peter’s MVIS Blog for his price calculator if you don’t want to create a spreadsheet. The numbers are getting rather silly. They may be reasonable, but silly when you consider that someone could’ve bought the entire company a couple of years ago at a ridiculous bargain.

LiDAR company market caps are measured billions.

Microsoft probably has high expectations for Hololens.

Within five years the global display market is expected to exceed $177B. Even a small market share is a lot of money.

Even without adding in miscellaneous and it’s possible to add billions to billions, for a company that was under $100M.

Oh yeah, and then’s there’s the Gamestop story, a headline and a community. So many of those investors have found MVIS that the MVIS discussion boards have gone from a few hundred folks talking amongst themselves, wondering if the company and the stock will ever be found, to almost 20,000 on the reddit board creating a cacophony of enthusiasm. It’s like going to your favorite pub to visit a few familiar faces, then finding the place has gone viral and it’s scary just trying to get in the door. Oh, well, that’s success, too.

Within one year the stock has gone from irrational pessimism to possibly irrational optimism. Or, has the stock not even reached a rational valuation?

The buyout will fix the price. If the buyout happens. Imagine working in a methodical mega-corp, trying to negotiate a deal for a $100M company that the investment community has driven to over $2B and may see no reason to stop until it is over $20B. Do you still buy out the company? Does the company need to sell? Are you now the only company that wants in?

MicroVision was complicated enough with its various product lines. Imagine the joyful mess if most of them become successful at the same time to a similarly large extent.

I don’t think the company will be bought out as a whole. There were many things to note in today’s conference call. I suggest visiting the various discussion groups (reddit, Fool, SI, IV) for better analyses than most publications produce. Allow me to note some language choices. (Hey, I’m an engineer, but I’m also a writer.) The CEO was suing plurals: clientS, partnerS, mergerS.

Multiple customers? Fine. That’s something most businesses consider a healthy thing.

Multiple partners? That’s what I heard. If so, good. Partnerships can work well, and not being tied to one is even healthier.

Multiple mergers? OK. Each gets only what they want, properly values it, and doesn’t value the rest at less than its worth.

The permutations are more than my brain wants to handle (at least this late at night, and for free. Now for a fee, well….nah.)

This blog is about personal finance, so I have to pick something to plan around. It is rare that everything succeeds. It is rare that everything fails. Last year the worry was that everything would fail, at least as measured by stock price. This year people are reacting as if everything will succeed, as suggested by price targets (that are as ambitious as the ones I had many years ago.) I am going to assume (cue the ‘assume’ jokes, but hey, that’s what we have to do) is that: 1) at least one product line will be sold off, 2) at least one suitor will become a partner, at least in part, 3) with the extra funds subsequently available, the company can proceed with at least one of the product lines independently. In such a scenario MicroVision doesn’t go away (which I prefer), is provided with a very healthy cash position, and may have substantial profitable revenues. In such a scenario, there isn’t one conclusive exit like in a merger or acquisition. Portions of the investor community will drift out with each product line spunoff, but others may be drawn in as the financial situation improves.

Will I be able to re-retire because of all of this? That’s hard enough to say, and it’s late enough tonight that 1) I’ll consider that later, and 2) won’t do anything about it soon because such a sequence of scenarios can take years.

As for the valuations, allow me to dream and recall another buyout I was involved in. Does the term “To Infinity and Beyond!” sound familiar?