Listening saves money? Yep. No investment insights, and yet, appreciating value.

I listened to a friend for an hour, and was thanked. I had a few days with good friends, which also meant sharing the time, and felt better than I’ve felt for years. And I also know what it feels like to speak and realize that none of the words found a home.

Yes. Yes. Listening is good. What’s the point?

Listening well can reduce some folk’s need for therapy, paid therapy, expensive paid therapy, therapy that has a time limit.

Have you ever had a conversation that went on for twelve hours? I wonder if there are any therapists who have that much time. The world is chaotic. There is always pressure to help the next person, and to save time for the therapist to have a life, also to recover from hearing a day’s worth of varied stories, some of which are dramatic, some of which are traumatic. I bow to their expertise and resilience.

Talking about mental health issues inspires many people to change the topic. Understandable. I enjoy listening to friends and feel privileged to hear their stories, and honored to hear the parts that they’ve never told anyone else. I also am human, not a professional therapist, so some stories make me back away – and encourage them to talk to a professional.

I’ve talked to professionals. Depending on how you count it, I’ve had a therapist about every ten years, usually for about a year. They have helped me (though I think I helped one more than they helped me. Hey, we’re all human.)

In 2004, I had chest pains. It was amazing how quickly I could get an appointment to see my regular doctor. I asked for an appointment within the next few weeks. They made a slot for me within a day. Lay down. Get an EKG. Wonder and worry about why they thought that was necessary. The doctor comes in, tapping a pencil on a clipboard. “This is classic.” I’m worrying that I’m evidently having a heart attack. He slightly chuckles. “This is classic. You have a perfectly normal healthy heart.” That was the joke. We knew each other. He read me well, or at least well enough. “Your problem is not in your heart but in your head.” He referred me to a mental health practitioner.

That’s a relief? Evidently there was some benefit to all that exercise masquerading as hiking, biking, skiing, and karate.

Six months of therapy sessions later I asked the therapist, “Am I crazy?” Yeah, it took me six months to work up the courage to ask the question. “No.” Whew. “You’re under a lot of stress with a very thin support network.” Whew?

I’ll paraphrase his general observation.

Fifty years ago, guys would stop at the bar on the way home from work. They’d vent to the other guys. Fifty years ago, women who weren’t working would get together for a variety of social and civic events, maybe with wine. Now, we don’t drink and drive, so that’s good, and there are more women in the workplace, which has its benefits. But we’ve lost the gathering of ‘like-minded’ souls who commiserate. Shared pain is diminished. Shared joy is amplified, but there seems, seems, to be less of that, lately. So, the majority of his clients aren’t crazy, they’re simply humans who need to listen, and occasionally, provide some advice. It’s more expensive than beer or wine, and it isn’t as frequent as the bar or the social circle, but it is what we have.

He helped.

A few years ago, the medical community declared an ‘epidemic of loneliness’. We have all those issues from things lost fifty years ago, but now people feel that social media and texts can replace personal contact. As a friend revealed recently, they feel a lack of personal contact. It isn’t sexual. It is hugs and handshakes. I get some of that through dancing, and I understand what they said. We got some good hugs in. I’ve got to get back into practice.

How much of today’s…dissatisfaction is people feeling alone, or cut off, or not heard?

So, I listen. When I’m doing public speaking I speak, naturally; but even then I prefer to begin before I begin by talking to people in the audience to hear what they want to hear. If I’ve produced yet another book, do they want to hear about the book, the writing process, publishing, or simply want to be entertained?

And then there are those quiet, simple conversations that start with no agenda but if allowed to go on long enough reach a point when significance is found. By then I have a good idea of how much to listen and how much to say. What I say has frequently been simply, “I’m sorry.” What I’ve learned not to say (though I do on occasion) is “So you should do…”

Recently, I admitted to my therapist that I was embarrassed to have nothing dramatic or traumatic to share. He grinned. Every conversation does not have to be dramatic or traumatic. Sometimes it is the simple things that are most revealing. Sometimes a conversation, even a professional one, needs a breath, a rest.

I’ve also mentioned to my therapist that, in times like now, they seem to be needed more than usual. He agreed, but I get the impression that he’s always busy.

And while I prefer to listen, I realize that when I’m in a session it is my time to talk. And I talk. Simply taking it all in and never letting something out is unsustainable, I guess. Maybe the pros can do it. But I’m happy to listen to my friends, and maybe talk some, too. No beer or wine or formal training required. Talk is cheap Ain’t that great?

Do you know that feeling when you’re walking along a ridge line with a thousand foot drop on either side? No. Of course not; few ever climb mountains. Yet, I suspect a lot of investors feel that way for the last few months. The market has carried them to new heights. They hope it goes higher, but the possibility of a drop is real. Fortunately for stocks, there are exits that don’t require falling off a cliff; and there’s a hope for catching a ride up another ridge.

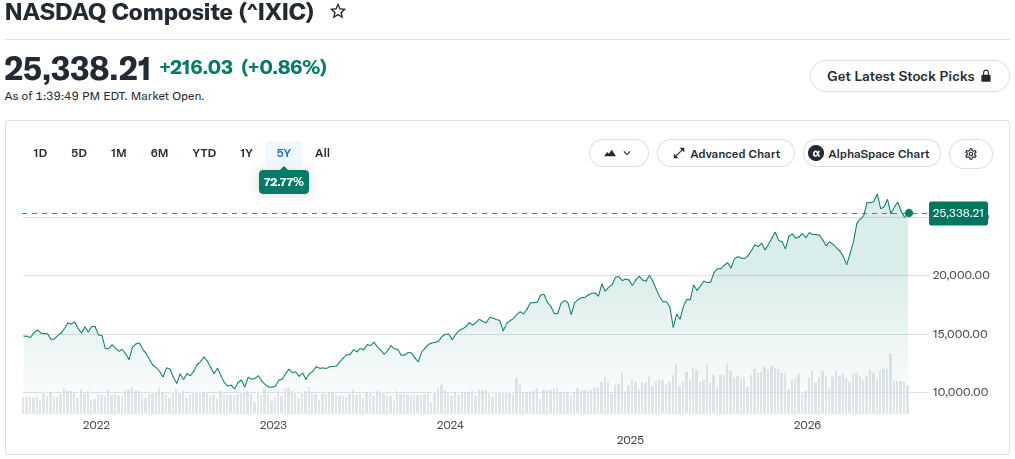

The stock market has been ridiculous for a couple of decades. Look for the blip that was the Internet Bubble and the Great Recession, and they barely register. Since 2016-ish, the NASDAQ has risen from ~5,000 to ~25,000 (as I type). A 7% rise is normal? Not lately. 5,000 at 7% in 10 years ‘only’ equals ~9800, not 25,000. 10%? ~12968.

Yahoo Finance

These are heady times.

These are worrisome times.

The financial news is worried about an AI bubble, probably for good reason. There’s lots of hype. Yay! There’s lots of worry. Boo. There’s also a lot of FOMO (Fear Of Missing Out). Continue on despite your fears! Don’t. If you’re afraid, listen to yourself, don’t discount your perspective. Ideally, find another one.

There is a fear of missing out, and then there’s a worry of finding a better or safer place. Some are already there with mutual funds and such. Higher expectation investors may hang on until the pop, or just past it. They can be big money, and when they sell they hunt for what I call lifeboat stocks, something to weather the storm.

The situation is that, when that big money bails, that community tends to bail, which then leads to scared money hunting for a home.

I’m not sure we’re there, yet, but the recent response to any good news from mega caps seems to be out of proportion for what the numbers say. It is as if a mob has quickly decided to hide from the rain by scurrying from under one tree to another. They may be off the ridge, but trees attract lightning.

In the meantime, regardless of their motivations and philosophies, the rest of us see the market making wide swings, sometimes to our detriment.

Several of my stocks are down significantly, yet most of the companies are making good progress. This seems to be based more on emotion than logic.

I’m glad I sold when I did.

QBTS hit ~$30. I hoped for more. I sold at ~$26(?). As I type, it is at ~$18.30. The stock is down. Their news is up.

LUNR hit over ~$45. Now it is at ~$12.25.

On a purely mathematical basis and expecting things to return to a norm, I should buy some more LUNR.

On a practical nature, I will hold onto cash because those are my living expenses.

Some are worried about the market. I worry about it too, but life is here to be lived. Besides, I have some health issues to deal with. (Groan.) Cash is a comfortable cushion.

Until the market gets off that ridge, or finds that the ridge truly does lead to something even better, there will be uncertainty, and this time I suspect the uncertainties are larger than usual. Maybe hanging on to the cash is a better idea than I realized. Maybe there will be some better buying opportunities, soon. Maybe nobody ever knows what’s going on, and investors will always be scurrying about. It makes for fascinating people watching.

Note: Here’s a post for those who follow stocks, but the same rules apply throughout life.

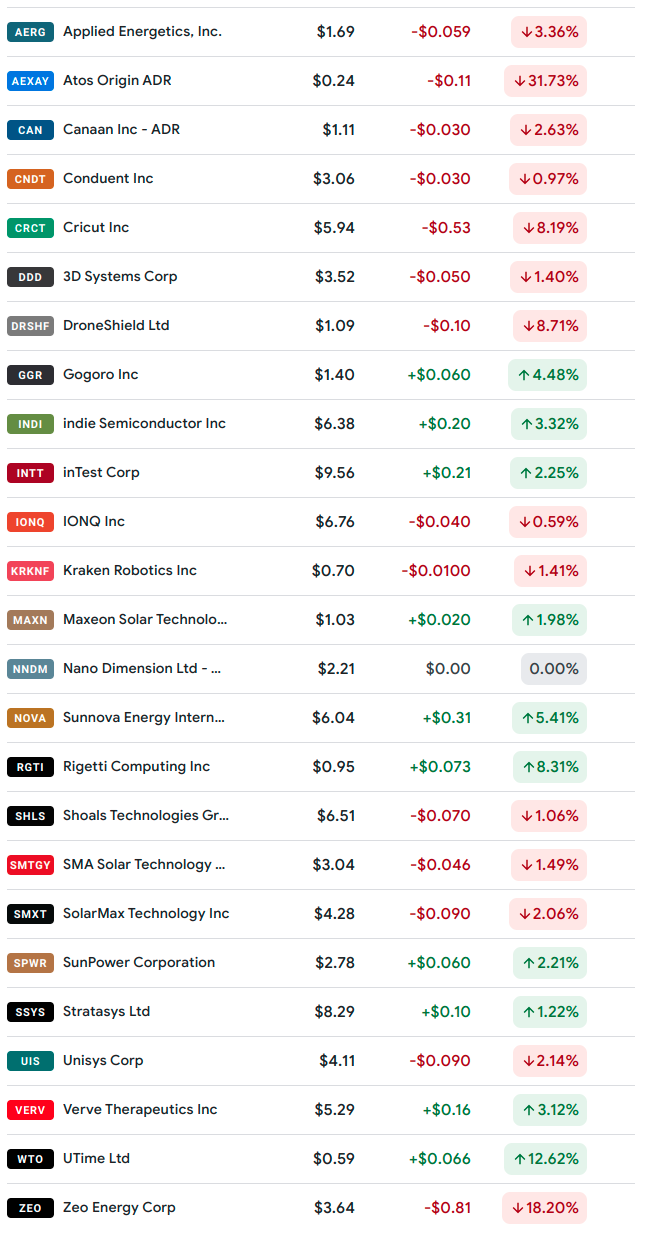

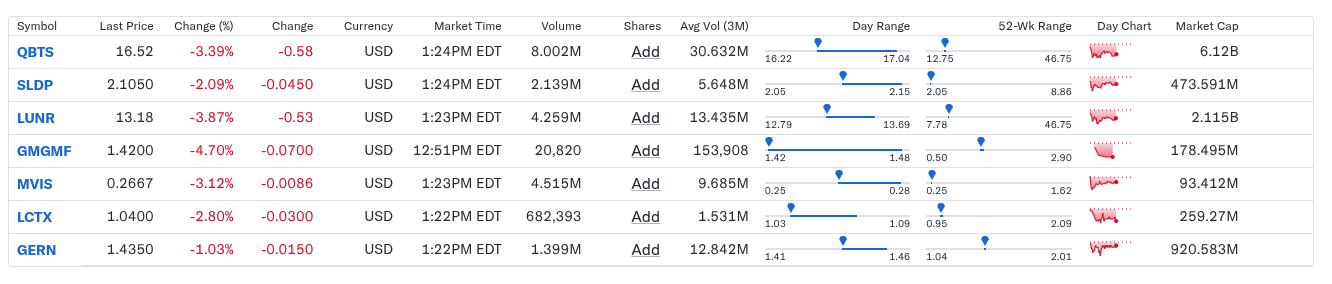

Google has improved their finance tool, now with AI! Groan. I guess it was inevitable; taking a useful service, hiring a bunch of programmers and a staff to maintain it, and then improving it until it is barely useful. Maybe by the time you are reading this Google will have corrected the errors it induced by changing something that didn’t need improving. Not likely, considering the history of improved products. Fortunately, there are competitors, some of which have histories, too.

For weeks, Google has been teasing a new AI-enabled upgrade to its Finance pages. Fine by me as long as I can turn it off. I track my stocks, or tracked them, by opening up a tab for my watchlist in Google Finance. Simple. The stock, its price, whether it is up or down, and with one click I could get financial data like market cap, and maybe news. (Some of my investments are in stocks that are so small that news is rare, but hence, more valuable when it appears.)

a Google Finance screen grab for years ago

The AI upgrade overwhelmed all of that, at least from what I can see.

a Google Finance screengrab from July 24, 2026

You’ve seen many screengrabs of Google’s Finance page in this blog. I’d like to create a new graphic of the old screen, but it’s gone. I tried grabbing a screengrab of the new graphic, but the screen is active enough that it sweeps a new news screen across the image instead. Not useful for tracking my portfolio.

Grumble. Gripe. Gripe.

Cheer and and and salute sites like craigslist that keep it simple and useful. I think their style will eventually come back into style, and all they have to do is nothing. Well done. Well played.

There are many other ways of tracking stocks and portfolios. I’m not going to list them. There are too many.

What I’m hunting for is simplicity, convenience, and of course, accuracy.

The data I want is simple, as I described above.

Accuracy is assumed, with some allowances for data transfer rates, which don’t bother me.

Convenience blocks out many sites that require regular log in sessions, drilling down to the key data, or bizarre formats.

Silicon Investor is a site I’ve used for so long (decades?) but predominantly for discussion boards. But, it keeps me logged in, and my data is available. Looks kinda kludgy, but it works.

screengrab from Silicon Investor

On a more official page, there is my official portfolio tracker on Schwab, which I rarely access because its security is justifiably tighter, which I appreciate. But logging into any system provides a risk of logging in incorrectly, which can cascade into a maelstrom of having to prove I am who I say I am. Great site. Nice service. But I only access it about once a week, not casually.

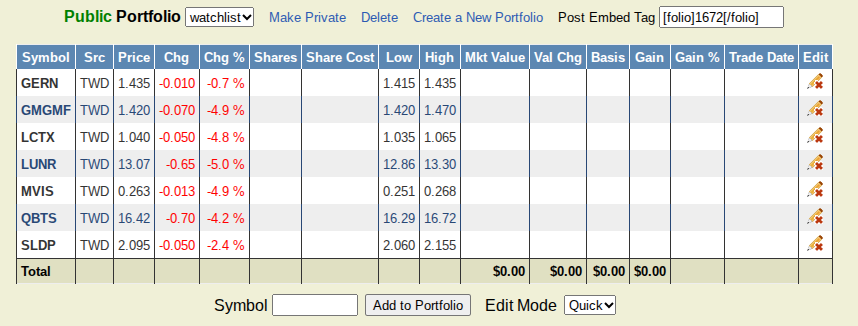

Whew. I just brought up Yahoo’s wikipedia page because I was about to refer to the company. Founded in 1994! Yeah. I knew it was old, back when any site was considered a success, and probably temporary; but I remember using it before Google (founded in 1998). Maybe they’ve maintained their simple style (and somehow survived years of drama). Ta da! They have. (Just ignore the realities of what they’ve been through. There should be a movie.)

Voila! Create a new account (because obviously it forgot the original one, or I did). Load up the stock symbols (while deleting all of their suggested ones that were ultra-mega-caps). And notice that it exceeds my expectations. They even include range data (and don’t worry if you don’t know what that means.)

screengrab from Yahoo! Finance from July 24, 2026

OK. I think I’ve found my new site to check regularly, for a while, until something else better comes along, and maybe not even going back to Google because this is better than that.

Craigslist, wikipedia, I do like such sites.

And I wonder if a minimalist, luddite-light, simplistic approach is about to see a resurgence.

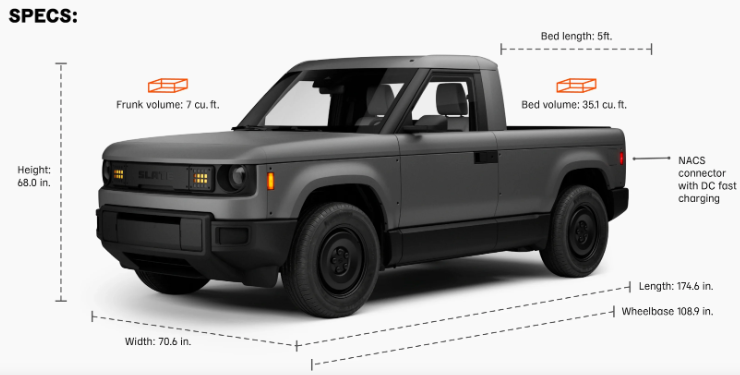

E-bikes are becoming more popular. EVs are potentially simpler than gas-powered cars. Have you seen the new electric pickup, the Slate? Simple, cheap, electric. Roll-up windows are back! There are far fewer systems to distract you from driving. If you want to modify it, then modify it. I want one (pending having enough funds and finding out how best to carry bicycles in the bed.)

screengrab from Slate.auto

Give me a simple car, and a simple camera, and a simple computer, and a simple life.

New does not mean improved, but maybe, just maybe, it may begin to.

Thanks for the years of service, Google. I liked you best when you didn’t want to be evil.

Pardon me as I dry my eyes. The World Cup proved to me something I’ve been looking for. Humans meeting humans is marvelous. Pundits and politicians don’t have a clue. You want the finance part of the picture? Imagine all the money spent on hotels, flights, food, and beer; and look at all the fun they generated. Imagine an economy run by having a better party. (Thanks, Rick Ingrasci.)

But, but, but…politics and AI and climate change and… And you’re right those threats exist. But they aren’t the only things that exist. Balance.

2026, the World Cup came to North America. I didn’t watch the games. I did, however, watch dozens of YouTube videos of people having fun with people. People got past the media summaries that are necessarily short sound bites. They got past the political statements that emphasize our differences. The people posted their videos of their lives.

The videos of their lives were of people realizing that the other people are people. Certain criminals claim the spotlight, and the media plays in to that. That’s news. The people posted fun, amazement, and wonder. That’s not news, but that’s far more important.

The media and the politicians are gatekeepers, editors of the world that filter the events into ‘simpler’ messages that hope to grab eyeballs and votes.

Have a better party. At least for a while, skip the news. Skip the politics. Dance, sing, talk, travel, listen, look at what you see, not what you’re shown.

Then, the kicker was that much of this was happening in the US. Foreigners who’ve only seen the country in the news felt betrayed. Sure, there’s bad stuff, but they celebrated a wonder at the country, not as a news item or political position, but as a people, culture and land that they could enjoy. I’m proud of us, and surprised and not.

Do we have flaws? Duh! Everyone does. Should we fix them? Yes. But we shouldn’t forget the positives. And, having traveled a bit, they do too, flaws and positives. We are humans. We have more in common than will fit in a news item or a speech.

As I mentioned, I watched dozens of videos. I’m sure there are hundreds, maybe thousands. Some were staged by YouTubers craving an audience, but many, most, were authentic.

My favorite was “America Hosted The Best Sleepover Ever”, which included an intro of “…The World Cup is just the US having a giant sleepover with the cousins we never get to see because our parents hate each other.” Just a bunch of people having fun with people.

Then I found a few others which were reaction videos. Reaction videos is where a YouTuber reacts to the video. These two were from different countries (Ireland and Britian?) saying much of the same. (~8 minutes each)

The parties were good and loud. The explorations were quieter and filled with wonder. Individual cities were called out, but I particularly enjoyed the ones from people who had the time to travel to small towns and to National Parks. I chuckle as I type because for each I’m thinking, ‘Oh, that’s good but they shoulda seen…’. And that was for our National Parks, of which I am a fan. Our state parks are pretty magnificent too.

They also showed us us. Texas is bold and brassy, just right for many of them. LA is warm sand and beach life. NYC is, of course, the most familiar from its size and movie exposure. They aren’t for me, but I respect those Americans and the way they enjoy life; and the visitors did too.

They were warned about murders and guns and so many other of our faults. They weren’t warned about our portion sizes, our diversity, our hospitality.

But, Tom, this blog is about personal finance. What does this have to do with that?

After social media gained traction (and after reading a few books like Powershift), I expected that a great movement, a great positive movement could arise from individuals. Individuals can now reach past the gatekeepers and spread messages that have been filtered out. Organizations have some control over global messaging, but they have significant competition now. Imagine a world where we have more and they have less. Imagine a world where positive messages eclipse negative ones. Imagine a world where criminals aren’t given the pulpit and the stage. What do you want to watch? What do you want to show the world?

But about the personal finance?

The world’s economies run on consumption, competition, and crisis. Imagine a world (and pardon the accidental alliteration) built from cooperation, creation, and compassion.

How much money was spent on all of these parties? In the same time, how much money was spent on bombs, bullets, and missiles? We’ll never get rid of both, but which economy would you rather see dominate?

And here I’ll get personal for you and me. What kind of business… What goods and services can we provide that fosters that other economy, the better party economy? B&Bs? Yes. Travel across oceans will almost exclusively belong to billion dollar companies (and I cheer my friends who’ve crossed oceans in sailboats). Food? Go local. Skip the restaurant in a box, decorations and menues included. What can you serve that you eat that is from your location? Thai may be great, but here around the Salish Sea I’d like to see more salmon and elk.

This may be a dream, but dreams come true.

My four main worries are AI, politics, climate change, and social injustice. I don’t use AI on purpose. I vote, but I don’t know of any party that matches my values. Climate change would be impacted by the travel, but not everyone has to travel, just enough to spread the stories. But social injustice, now that may be best assaulted by people treating people as if they are people. They aren’t labels or stereotypes or races or genders. They (assuming AIs are sentient yet) are people, flesh and blood, trying to get through life and maybe even pursue happiness.

Pursue happiness? Sounds like a fine business opportunity. I wonder how I can invest in it.

PS I watched a video from a local news channel. They acknowledged the trend, and then spent a quarter of the time describing all the bad things that happened. Sigh.

Just a short note to mark my purchase of some more SLDP.

SLDP is part of a trend I expect to do well, solid batteries. Scroll through enough videos of fires from lithium ion batteries and see a need for something safer. Read enough headlines about the difficulty in sourcing lithium and see a benefit from using other materials. Check the research and notice the benefits in operational things like charge times and see a draw to switch from lithium ion batteries to something better.

I don’t know that SLDP will be a winner, investing entails the risk of loss, but welcome to the world of investing in innovative companies.

Battery technology may seem static but it hasn’t been. Like any other technology, someone is usually trying to come up with something better.

I won’t bore you with the detailed history, but a casual glance shows that those early batteries would not fit inside your cell phone.

I am old enough that I remember when batteries were just called batteries. Then came alkalines. Then there were things like Ni-cads, but I didn’t worry about them. I just wanted my AAs and AAAs. I knew about lithium ion, and started to pay attention when cars were built around them. For me, it is natural to wonder what’s next.

More range. Smaller packages. Quicker recharges. Safer. Lighter. Cheaper. They’re all good. I read claims about all of it, but know that the market simply needs something better in some way, anyway, to generate a new product.

The firms have advanced from talking about lab work to prototypes to test articles with hints of production runs within a ‘few’ years. Cool. Fine. Good. I’m patient. I buy now.

I also buy now because I’d rather be too early than too late. I also buy now because I recently sold some QBTS. That is largely for spending money, but I tend to take such opportunities to reinvest. SLDP is down, more than half of where I bought it last year. I could buttress that position up to my personal version of a share limit for what may be cheap.

After I realized that SLDP was cheaper and that the company was making progress I started paying more attention. I noticed my reaction that I was paying more attention than normal. For me, that much attention can be a waste of time if nothing is done, and it can be a sign that part of me intuitively feels (not an investment term) that I should do something.

So I bought. I bought a bit. I also am comfortable with the purchase because purchasing a stock is not a lifetime commitment. I rarely sell, but I just sold some QBTS, so there’s proof that I treat the stocks as assets, something fluid and liquid, and those are interesting terms when describing something solid.

It isn’t hard to imagine batteries progressing to the point that they are more like a lifetime purchase. Smoke detectors now come with long-life batteries. It has begun. Appliances now come with embedded batteries, partly to boost the power of electric kitchen appliances, but also as a backup in a storm. Cool. Go a bit further and off-grid applications become even easier. Cars and planes may never get there, but a 600 mile battery that charges in thirty minutes would be a game changer for someone.

I hope I can afford them.

In the meantime, I bought some SLDP for less than $2.50. Now, I sit and watch and wait, and more importantly, get on with the rest of my life.

Happy 3rd of July! Hey, it’s a compromise between July 2nd (John Adams favorite) and July 4th (a date that 46% of Americans celebrate without knowing why.) Whatever, it is also the 250th anniversary of America’s declaration of independence, frequently spelled Declaration of Independence. It is also my 50th high school reunion. My ancestor and signer of the Declaration, Francis Hopkinson, may groan in his grave, or not. Maybe this is the way they wanted it to turn out.

If you want a primer on the Declaration, or want to hear my voice, here’s my rendition of it. (Let’s see if it uploads and downloads.)

What to talk about first: family history from 1776, personal history from 1976, or current history from 2026? Maybe some insights, because why else write a blog post? (Of course, it’s Friday, so I guess I’d do that anyway.)

Francis Hopkinson, founding father, or at least a guy who showed up for work and ended up signing a piece of paper. Haven’t heard of him? Why would you? Half of Americans don’t know July 4th 1776 was a thing, an event, one could even say something that was revolutionary.

Founding fathers are mythologized as if they were infallible. Some think so, including politicians. They didn’t. They knew they were people, granted they tended to be rich, white, land owners, and their own version of religious, but people, not heroes or icons. That’s common with heroes and icons. I’ve read some of history. Thanks for doing what you did, but I’m not surprised that no one ordered up a halo for him.

It was a revolution. Some say it was The Revolution, but a lot of the world agrees with the almost half of Americans who can’t see back that far. That something that revolutionary can be lost is a source of pondering, at least for me.

But hey, it’s worked this far, sorta kinda. (If you want a recent upbeat view of the US, go to YouTube to watch some reaction videos from the World Cup. Many foreign visitors are pleasantly surprised at the reality of the US, especially as compared to their media coverage and political commentaries. Residents can rely on personal experiences for personally real realities.)

Again, thanks Francis. (By the way, family folklore has it that the folks in the UK call him the traitor. So it goes.)

So, by luck of birth, I graduated high school in 1976 from West Mifflin South High School. Go Spartans – and they’re gone. The building was knocked down a few years ago. It was more modern than the WPA building next door, but it’s gone. I suspect the WPA building is gone, too. There were probably good, bureaucratic reasons for the demolition; but, I prefer the neighborhood folklore version which was that it was above an abandoned coal mine that was collapsing. The other bit of folklore was that it was collapsing because someone was sneaking in and taking out support timbers to use as firewood.

We were graduating, which should be a celebration, and it was; but, I recall a great contentious debate about our tassels. On the top of our graduation outfits were the cap in the ‘cap and gown’. The caps had a button on top. Around the button was affixed a tassel of yellow/gold that represented one of our school’s colors of blue and gold. Ah, but it was 1976, so someone decided, decreed that the tassels should be red, white, and blue. Think politics in the schools is a new thing? After months of testy debates, we students got to pick from ourselves. I picked both.

And now that episode is mostly forgotten, except maybe at this year’s 50th Reunion. I didn’t attend. Something about living 2,600 miles from home. I don’t miss the place much. Most of my friends have moved away. Some have popped up on social media. I miss the definite weather, four seasons: Winter, Spring, Summer, Fall; as compared to Western WA’s relatively reliable blandness. Though, around here, a one or two hour drive can land me in a greater range of climates. I miss the lightning storms. So it goes.

I understand that the politics there are as confused as anywhere.

In the bigger 2026 picture, there’s the 250th celebrations, and the Soccer World Cup. And fireworks. And pride. And concern. And optimism. And pessimism.

250 is definitely worth noting. Pat ourselves on our backs, but really, pay respects to the Founding Fathers who got this started, and the generations of sincere-yet not-always-qualified people who have maintained the country, even when it had to be stitched back together.

We grumble and gripe, and usually for good reason.

“…it has been said that democracy is the worst form of Government except for all those other forms that have been tried from time to time.” – Winston Churchill

Of course, whether we have a democracy, or a republic, or a democratic republic, or a representative whatever, or an oligarchy, or… Go ahead, debate it amongst yourselves. We’re celebrating 250 years of something. Did Francis guess at this? Did 50% of Americans not know about the reason behind the 4th? (Cato Institute) What do we have now? I’m not answering that because my opinion is mute. I can’t even get the hospital to listen to me, why would my government?

We vilify the ‘others’. Worldwide, the media and the politicians do too. Considering the current politicians, there’s a lot to vilify.

And then the World Cup happened.

The general consensus is that the world is pleased and surprised that Americans are nice people, as if their people aren’t. I’ve traveled a bit, and I like them, too. I like people who treat people as if they are people, which works, because they are, we are. The media and politicians, however, need headlines and sound bites. Headlines and sound bites need to be dramatic.

Drama is by definition, not mundane. And yet, the majority of our lives are not dramatic enough to make headlines. For many, life is just Not mundane enough to be interesting. So, when people (soccer fans) meet people (locals) their lack of personal melodrama comes across as a massive positive – which it is. Without the media and the politicians, we can have fun. Fun. What a concept!

There’s red, white, and blue on the flag. Wave it, if you want to.There are headlines and sound bites. I’ll read and listen, sometimes only as a distraction. There is drama and there is strife, but we are also here with each other. Why not accept that almost all of us are people being people? Good enough for me.

Let’s see. The simplest review is: in the most recent six months:

GERN is down ~3% LCTX is down ~21% MVIS is down ~60% GMGMF is up ~7% SLDP is down ~39 % QBTS is down ~8% LUNR is up 31%

Eep, but then, the previous six months were so good that it would be surprising (though wonderful) if they kept up that pace. After expenses and taxes and such, my net worth is down, but only about ~11%. In today’s chaotic world, that feels like within the error band, especially considering the previous period being up over 100%.

Social Security continues to pay. Good. My Boeing pension continues to pay, but just for a storage unit. Business sales (books, talks, photos, consulting, et al.) basically stopped for the last two years as I moved from Whidbey Island to Port Townsend. Really, relatively stable.

As for reality, it does not feel relatively stable.

AI has been slowed, but even at its pace, I’ve heard a projection that an AI should be able to launch an unsolicited viral social media and virus campaign this Autumn, which holds with my educated guess. I think it is already ready.

Climate change continues to change, and doesn’t care if certain humans deny it. I’m glad to see the global acceptance of wind, solar, tidal, current, and geothermal techniques. I’d probably get an EV now, but 1) my trailer park may not be able to carry a larger charger, and 2) I’m waiting on the solid-state batteries which may come soon, and 3) my knee surgery is occupying my mind in the meantime.

Politics are failing, which can be a good thing if we replace them with something new, just not the other party because it’s another party.

Social injustice issues are being countered by current administrations, but they’re gaining momentum regardless, and may accelerate as elections provide an opportunity for change.

And, aliens, because there’s always a chance of things like aliens that may redefine everything.

But what about my investments? I am an amateur futurist. I feel compelled to consider alternative futures. I am also a realist. Tomorrow tends to be like yesterday, until it isn’t. Until then, I invest in companies working on advancing industries. Things will continue to change, and that doesn’t change. I won’t share (rant) about the various prognostications I’ve made which were laughed at way back then that came true. But that is also because many of my prognostications were also wrong. (The US hasn’t officially fractured – yet.)

A luxury would be being able to let my investments ride, ignoring market fluctuations. Yes, I have Social Security and my pension, but growing my net worth requires funds from somewhere else: stocks, my business, good fortune, etc. I am in considerably better financial shape than I was before I sold my house in 2024). My asset cushion has grown from several months to several years. (And has been an interesting lesson in the trap of ‘more’, as well as a reality check on how much more I need to buy a house and its land. More.)

I hope Medicare lives up to its promise and takes care of my knee surgery. I hope my investments recover from the asset redistribution that was folks (or AIs) selling LUNR to buy SPCX (SpaceX). I even hope for my books, photos, talks, and gigs to generate income. I also hope I don’t encounter unexpected expenses. (Don’t we all?)

So, things have slipped a bit, but not horrendously so. My stocks are still in companies that have significant potential and are potentially undervalued. And I trust to good things happening, significantly good things.

And, I still buy lottery tickets.

Wish us all good luck for the new year, and if it is a happy one that will be a bonus.

Read on for my stock synopses. And good luck.

INTRO Here’s my semi-annual exercise to see if I remember why I own the stocks I own, and so I can check back and see if their stories have changed. I post in case it helps others too.

Geron

GERN (market cap is $0.821 B was $0.875B)

Geron is a biotech firm that has a treatment based on telomere management for blood disorders. The same technique may be a lead into other ailments. For years, the company stated that they intended to extend human life (hence the name Geron of gerontology), but most of those assets have been sold off to generate cash. It’s one treatment has been FDA approved, but has had limited commercial success, though that may be a marketing issue and not a technical one.

The company has promise, but less than when I initially invested in them more than twenty years ago.

I look forward to developments and positive patient reports.

DISCLOSURE LTBH since 1999 and continuing to hold, but do not plan on buying more unless I see significant positive changes at the company.

I continue to hold because selling so low has little benefit and I am an optimist.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/

Graphene Manufacturing Group, GMGMF for short, is a small company developing solutions through the use of graphene. Graphene had been an academic and lab curiosity, but GMGMF has recently claimed to have sold coatings and such that use it to improve the efficiency of HVAC systems.

I do not expect the HVAC coatings market to be large, but cash flow is handy, and so is the name recognition. I suspect the company’s products will be better known within the technical side of customer companies where word travels mouth-to-mouth, which I won’t witness. I am more interested in their solid-battery work, which is early, though trending towards development within a couple of years.

DISCLOSURE I tend to LTBH, and have held shares since 2024.

Circa 2023, I produced a video about the company on my One Company One Story YouTube channel.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/)

Lineage Cell Therapeutics

LCTX (market cap is $0.326B was $0.380B)

Lineage Cell Therapeutics, LCTX in shorthand, is an innovative biotech with several products in work. I am familiar with them because of their treatment that uses stem cells to regrow nerves, but am also aware of their work in treating Macular Degeneration. In some ways, they are a mini-conglomerate as they have multiple potential product lines.

Their ability to regrow some nerves in accident victims and in age-related (?) macular degeneration is proven in early clinical trials. Competitors exist, sometimes using mechanical aids to accomplish similar results. I prefer the cellular approach, but the regulatory approval process may make the mechanical approaches easier and quicker to reach approval.

DISCLOSURE LTBH by habit, but having to remember that my LCTX/BTX holdings came from AST (2014), which was spun off from GERN (which I’ve held since 1999). I hear patience pays, but it is easy to have doubts after twenty years of waiting.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog https://trimbathcreative.net/

Intuitive Machines (LUNR) is an aerospace firm that is active in space commercialization and colonization. Simply based on my perception, they seem to be more involved in the infrastructure required to establish sustainable operations in space, and in particular, on the Moon. Competition exists, but this is also a market where backups and redundancies are more than recommended.

Having landers fall over is not a good look, but as one post pointed out, they hit 85% of their success criteria even when their lander fell over. Space is risky. The Moon is far away. This work is activated by remote operations. And there are those competitors. They have, however, broadened their service base, and may have improved their financial situation. They aren’t alone, but they are well positioned.

DISCLOSURE LTBH since 2024. Bought more, recently.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/)

MicroVision

MVIS (market cap is $0.112B was $0.277B)

Oh dear. Am I doing this again? A new CEO? A new direction? Sigh. Back to basics.

MicroVision, MVIS, is an electronic component manufacturer. They are currently being known for their LiDAR sensors, which had been directed towards car manufacturers and others. They had been known for using that same tech, an oscillating mirror on a chip, as a sensor or a projector or both, to create and read optical information. Think of an always-in-focus display that is small enough to fit in a smartphone or a pair of glasses. The LiDAR sensors are also cheap, small, and possibly robust.

MVIS’ products always sound positive, disruptive, innovations, yet for 30 years the company has yet to develop a profitable, sustainable product line. They’re very good on promises. Each CEO has a new set of promises as if the previous CEO or set of promises were flawed. After over 20 years I remain fascinated by the technical possibilities, but wonder if there is an inherent and un-spoken challenge that the shareholders are not being made aware of.

DISCLOSURE LTBH since 1999 (though the very first shares are gone). I continue to hold because the price is so low that the only benefit to a sale may be for tax losses, and because, if only by luck, I think the company may be profitable because a customer wants the product regardless of what management has in mind.

Dilution means that I no longer have more than enough if the company finally succeeds and the stock reaches the heights I think are possible. Some day, some day…

(I’ve also collected links to the other discussion boards and my other stocks over on my blog https://trimbathcreative.net/

For even more details, follow my blog’s tags for MicroVision and MVIS, which reach back a decade.

D-Wave Quantum, aka QBTS, is a small, leading edge, quantum computing technology company. They are receiving recognition for actually producing products and services into a industry that the industry leaders say is years away. QBTS doesn’t seem to care and keeps making products (and profits?) anyway. There are competitors, but one source of my optimism is that the field of ‘quantum computing’ is differentiating itself into a variety of applications. This seems to me to be similar to Intel having so much work to do that a variety of small, innovative companies developed similarly profitable products. This may not be like that, but it could be.

QBTS has gained enough recognition that they are frequently included in news articles about quantum computing. Big firms still get the interviews and emphasize their need for big projects, while QBTS simply gives companies and organizations what they want and need without as much showboating.

Of all my investments, I am most optimistic about quantum computing because it may become more ubiquitous. I hope QBTS continues to play a large and profitable role.

DISCLOSURE LTBH since 2024. Sold some shares to cover my investment. Sold some shares to realize a profit. Sold some more shares to realize a profit because that’s one way I pay my bills. Holding the rest because 1) they’re all profit, and 2) if QBTS succeeds as much as it could, these shares could look cheap, maybe.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/)

Solid Power

SLDP (market cap is $0.584B was $0.857B)

Solid Power (SLDP) is a startup working on solid-state batteries. Finally, a name that makes sense. Solid-state batteries have advanced to the point that they’re coming off the lab bench, and the prototype production line, and are waiting for The Large Client. The potential is there (quicker charging, safer materials, fewer foreign interruptions, etc.). When some large firm or organization places a significant order, the stock could have a significant and positive response.

As with many new technologies and industries, there are many companies computing. Also, there is uncertainty about the size of the market. That is one reason among many of why this is a speculative stock and company. Risk/reward, reward/risk; if we knew what worked, this would all be easier.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/)

For more details about the stocks, here are links to various discussion boards where you can find my synopses, as well as others’ points of view. For more details about how I do what I do, there’s a book that I wrote at the request of several friends: Dream. Invest. Live. Maybe you can help my personal finances by buying a copy – though the frugal part of me recommends checking one out from a library.

Many of the independent investors who contribute to the discussions provide in-depth analyses that either aren’t available elsewhere, or would cost too much to buy. The other advantage is the diversity of perspectives. Unfortunately, I don’t engage as much as I did before. Some discussions have degraded due to lack of moderators, or overly zealous moderators (immoderate moderators, an oxymoron), or have too many immoderate voices. Some boards are effectively ghost towns, or feel like cavernous empty warehouses.

“Gold mines produce far more rubble than gold. It is easy to complain about the rubble. Ignore the rubble. Pay attention to the gold.”

Regardless, here are the sites I continue to visit, even if it is only to lurk and listen.

I encourage you to tune in, because more voices (as long as they’re mature) make for a better conversation. Maybe I’ll read you there.

Investor Village (widest range of boards, could benefit from more traffic)

Whew. I’m saying that a lot, lately. I winced because I didn’t sell QBTS at $30, but got some out at $25. Now it’s in the $22 range. I moved two years ago, which was good timing. I left Boeing in 1998, which was even better timing. Precise timing is a wonder, but a bit of imprecision coupled with patience can work, too.

It would certainly be nice to know the exact time to do the right thing. If that’s happened with me, it has been through luck. The decision usually involved some intellect and research, but the exact timing was a guess at best.

I’ve been reflecting on timing as the time comes for my Semi-Annual Portfolio Review, which is arbitrarily due next week at the end of June. I’ve also been reflecting on this observation in last week’s post.

“Ironically, of the seven companies valued more than SpaceX, five are very familiar in my life: Apple, Google/Alphabet, Microsoft, Amazon, and Facebook/Meta. But they all started as much smaller companies.”

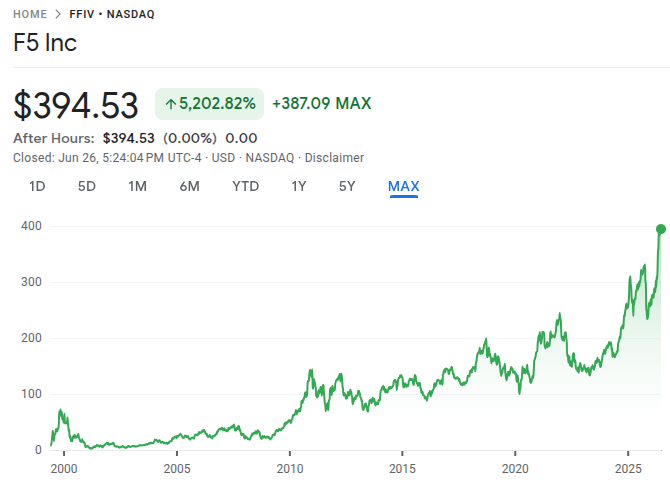

Early in their trading histories, I owned shares in Apple and Microsoft, as well as Starbucks and F5. I’ll spare you the longer list. I sold them all. I sold them because I made a profit and needed the money, or at least had a better use for it at that time.

F5, aka FFIV, was sold at ~$40 to pay for a downpayment on a house. I bought some at ~$4. Today it is just under $400. I made a ten-fold gain. I missed out on a ten-fold gain. A bit of patience and I could have bought that house for cash, except the rental I was in was actively damaging my health.

Google Finance

I wonder how my life would be if I had found a better rental in the interim. I may have never had a threat of foreclosure which prompted anxiety attacks and existential scrambling.

The same is true of all the stocks that subsequently did as well. If I’d hung on, my finances may have been much better, various health care issues could have been resolved when they were smaller, and life may have been better.

Or not.

I’ve also held on to some stocks for decades, which have turned into dead-ends, so far. I continue to have hopes for GERN, LCTX, and MVIS, but ‘hope’ is not a strategy. If I sold today, there’d be lots of losses.

And yet, as I’ve noticed before, the most I can lose in a stock is 100% and the most I can gain is thousands of percent. Put $10,000 into a stock that goes to zero and have zero (as well as tax losses, which can be a benefit in some portfolios.) Put $10,000 into a stock that goes up over 1,000%, and I’ve gained ~$100,000. At that rate, such a gain in one stock can cover ten losses.

But there are no assurances of gains or losses or the appropriate timing.

Finances meant I had to sell my house two years ago. Life’s been better since then, mostly because I got rid of a mortgage. Stock performance couldn’t bridge the financial gap, then.

I left Boeing in 1998, just as the merger with McDonnell Douglas was about to change the culture. Stock performance meant I could as we were about to become millionaires. Of course, if I’d stayed, my salary and benefits would’ve had years to grow.

Decisions made then necessarily have consequences not seen until later.

Most of my stocks have had a turbulent month. Let’s unscientifically blame

SpaceX’s IPO. SPCX has a market cap ~$2T. 2 Trillion Dollars. Two Trillion! Congratulations! That also sucked up money that had to come from other stocks. Companies that are making progress, and possibly making money, had their stocks go down because investors didn’t want to miss out on SPCX.

Oh, woe is me?

Nah.

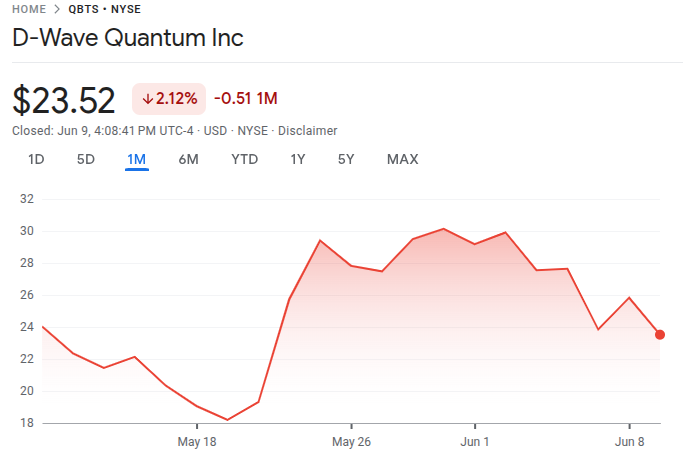

QBTS hit a near-term high of ~$30. I hoped for more, and watched it drop to $25. The timing wasn’t precise, but worrying about the precise timing was only a hope, and was a waste of time. Time is precious. I don’t ignore the value of my time. I sold at ~$25. Now it is about $22. I didn’t maximize my profits, but 1) I’m not going to complain about an investment that went from <$2 to >$20 in 2 years, and I still have stock in QBTS, so I’m still in that game.

But QBTS is not in SPCX’s business. Space investors were more likely to already be invested in space stocks, like LUNR. LUNR peaked at >$46 and is now <$20. Ouch.

So, here I sit wondering about my timing, and remembering history. Ignoring the last few weeks, where do I think these companies and their stocks could be in five, ten, twenty years? That’s enough time for quantum computing to become normal, a lunar economy to be established and growing, and most of my other stocks to have progressed to profitability. Holding onto these stocks now can be a significant benefit then, for various definitions of ‘then’. MVIS could even get a customer! Imagine.

It is easy to get caught up in the financial equivalent of doom-scrolling. People laughed at AOL, which I bought at ~$1 and sold at $40 after it passed through $80. Given enough time, long-term projects can accomplish incredible things. (BTW I’m glad I got out of AOL as they merged with AT&T, but that’s another story.)

As it is, I hope I have sufficient finances to cover my expenses for the next several months, ideally a year. Within that time, the furor over SPCX will probably abate, as it already seems to be happening. My various stocks may recover and then surpass their recent records, and my cycle will continue. Fine.

(Assuming AI, aliens, climate change, politics, and social unrest don’t flip the playing board.)

Was the timing of my stock sale precise? No. It never has been. Fortunately, with that sale, I can now afford a bit of patience. (Maybe I should buy some LUNR if it drops much more. Hmm.)

As I type, SpaceX’s stock puts the company at a valuation of $2.43 Trillion dollars. A laptop screen can have a variety of sizes, but 2 Million is common enough. Let’s round SpaceX down to $2 Trillion. Each pixel could represent a million dollars. One pixel being enough to retire on. Make it two. We’re talking about numbers that don’t make sense. Let’s try to make sense of them.

Regular readers know I tend to buy stocks in companies that are worth less than $2 Billion.

If I buy stock in a company that’s worth $100 Million and it becomes profitable, it is not a surprise if it becomes worth $1 Billion. A nice ten-bagger.

Fund managers are business people, and they minimize their costs by buying big companies where they don’t have to worry about the SEC and becoming large fractional owners. They tend to ignore small companies, which works to my advantage.

If I buy enough stock to own 0.1% of a company, and it becomes a $1 Billion dollar company, I become a millionaire.

There are more reasons to buy small companies (supporting positive disruptive innovation, etc.) but those are the ones that come to mind as investors are buying a stock that starts life as a Trillion dollar company.

Unless you’re buying into a stock for eventual dividends, or glamor value, it can be risky assuming that it is going to grow much.

Having written that, I also didn’t buy stock in Amazon, Facebook, Google, and several other mega-corps because I thought they were too expensive and too popular. They were, and I still hold to my strategy of buying simpler companies, but they IPOd at relatively low enough prices to have room to grow. And they did. Congratulations.

Fundamental Questions: How much bigger can one of the biggest companies become? How much room is there for the stock to rise?

My current stellar performers are LUNR and QBTS. (Market caps of ~$5B and >$9B, respectively.) At various times since I bought them, they have risen ~2,000% – 4,000%. If SpaceX does that, (2.4T x 2,000%), it will be worth ~$50 Trillion. Nvidia is >$6T. SpaceX would have to redefine the limits. Someone’s billboard will need yet another digit.

Ironically, of the seven companies valued more than SpaceX, five are very familiar in my life: Apple, Google/Alphabet, Microsoft, Amazon, and Facebook/Meta. But they all started as much smaller companies.

Fine. Good. Big money is practiced at chasing big money, and big money can make the job less about goods and services and more about lobbying and exploitation.

So, a rocket company is now larger than car companies. It is even bigger than mega-beneficiaries like defense contractors, and most energy companies.When does hubris kick in? I don’t know.

Looking back from 2026, I bought into MSFT, AAPL, ORCL, AOL, PIXR, SBUX, etc. when they were fairly young, the 1980s through the late 1990s. Big names, but they all started small.

(Gee. That review makes me feel better about what I got.)

So, I’m not going to tell anyone to do anything. I just write about me.

I am going to watch SpaceX, not to buy anymore, but that one stock has sucked up over $2T in investments, and a $2T shift in the market is hard to ignore, especially when it’s influenced by an ultra-oligarch whose goals are mercenary.

What I am also going to be looking for are those companies that will linger in the sidelights, letting all the publicity play out in the rocket-fueled limelights. I suspect there are some good candidates there being overlooked, and underpriced. Imagine how good they can do and how much they can grow.

Oh, to have the luxury of patience. I still have plenty of cash, and now I have a bunch more. I sold a bit of QBTS, not because I had to Now but because I’d have to eventually, and it seemed like the market is sliding. I’m glad and sad that I did.

I tend to buy or sell stock about once or twice a year. I may watch the stocks daily, sometimes hourly, but that’s because I find companies’ stories to be more interesting than sitcoms and scifi. (And I write scifi!) My previous sale of significance was last Autumn. We’re nearly to Summer but I decided not to wait.

As I mentioned in my previous post, my innovative company stocks were depressing as the market runs into uncertainty. In my opinion, most of those companies are doing what they should be doing, at least technically. Considering the emotions of the market, the economics depend more on subjective terms like confidence and worry. I can’t evaluate those as well as the more objective criteria.

As I posted in I Shoulda Coulda Didna Sold, QBTS was one of my candidates to sell for some cash. Sell a bit. Still have a lot left. Wait out the weather in the market.

I woke with the market, by accident, serendipity, or luck. QBTS was up! Great! Sleep a bit and hope it gets higher. Maybe it will recover, but sell a bit because a cash cushion is one of my most reliable luxuries. Get up. See it dropped. Sigh. Get out of the bedroom and to my ‘office’ (hey, it’s a tiny house, so definitions need to be redefined) and see it’s dropped some more. Sell some, even before making breakfast because this is evidently on my mind, and another luxury is a less cluttered mind. Fine. Not as good as last week, but good enough.

I bought the shares at ~$0.75. I sold them at ~$25. Quit complaining. Optimizing is partly based on luck, so don’t go claiming some ultra-intelligence. As I type, the stock bottomed at just over $22. Last week it was at ~$30. Swings!

Stocks are not eternal commitments. For me, they are investments. In this case, I bought some because I believe/estimate/hope that quantum computing will become a major industry. It may not hit the home market, but 1) many said that about PCs, and 2) even if quantum computers are only accepted in organizations, they can still be a major business. I hope.

‘I hope’ is not a strategy. But this wasn’t purely hope and a gamble. I’ve witnessed several technologies that people laughed at which then did well. (Search this blog for SBUX.) AI seemed to be a bubble, so I steered clear. It also seemed to encroach on some ethical boundaries, which made it easier to look elsewhere. A fundamentally new approach to computing seemed, and seems, due.

I can’t find my notes from my first purchase (typing this in a coffeeshop) but the market cap was < $1B. Now, QBTS’ market cap is $8.7B. In ~ two years, that’s a good investment. That is good news but also a cause for caution. How much higher can it go? QBTS is not the only quantum computing company. There is some upper limit to the size of the industry. There is some upper limit to the price of the stock. I suspect the market has yet to define either. I also suspect the market can enter a period of irrational exuberance when the technology looks proven, the applications become clear, and masses of investors decide they don’t want to miss out. Folks selling AI stocks now may be looking for The Next Big Thing and park that money here.

Whatever.

It is easy to watch the ticker and focus on that day’s bumps and squiggles.

The stock is down, for a day.

The stock is down, for a week.

The stock is basically flat, for a month.

The stock is basically up over 30%, for the last twelve months.

The stock went from <$1 to >$23 since I bought it about two years ago.

Pick a perspective.

What will come next: a fall, a rise, or something that fits someone’s narrative in the middle? I don’t know. I know I’ve made a profit, made some cash, and still am invested in a burgeoning, innovative, positive, and disruptive technological company. And I have have some cash. You see, there’s this knee operation coming up, and I’ve started to see the bills. Eep! Glad I had some stock to sell.