(Disclosure required because I’m writing about real estate: I’m a broker at Dalton Realty, Inc. http://whidbeyrealtor.com/. Not a plug for my services, but evidently you know where to find me.)

One big thing makes me think about bigger things, and I know I can only know a part of the story. Later this month I’ll make my first public presentation since the pandemic began, the update to my somewhat regular talk about real estate and affordability on Whidbey Island. (The Ever-Changing World of Whidbey Real Estate) The local libraries are starting to open up for public events, again. I get to be one of the first. Public speaking returns! Thanks, Langley Library and the Sno-Isle Library system. Thinking about that local story made me think about the larger story, which could be a presentation, too; but can also be a blog post here. Affordable housing and the sustainability of the real estate industry, there’s yet another place where the New Normal is being sketched in.

It is easy to assume that real estate news is only happening where you live. Everywhere must be different, right? Sometimes yes. Sometimes no.

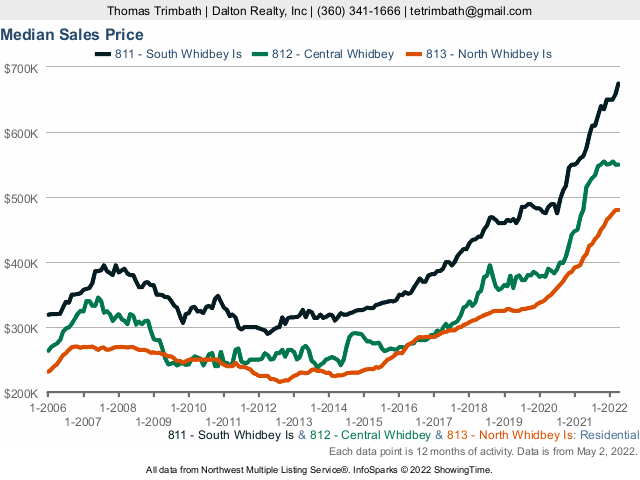

In the previous year, real estate prices where I live (Whidbey Island) have risen about 15% to 19% depending on the part of the island. Those percentages are a worry. The island has been seen as unaffordable for years. Rather than temper that, the pandemic accelerated the trend. With price rises that exceed historical norms of a few percent it is easy to assume it is an isolated incident, maybe a consequence of city folks escaping to a place where there’s more room between people. (Rural Distancing)

It isn’t only here.

Here are some sketches of my opinions.

Inventory is down. Twenty years ago people were more mobile. Families grew and shrunk. Upward mobility was followed by downsizing. Kids moved out, started families, and started households. Repeat. The Internet Bubble burst and 9/11 didn’t help. Instead of switching addresses every 6 or 7 years, people stayed in one place longer, like 10 years. The Great Recession hit. (The Second Great Depression in my opinion.) The typical length of a stay became more like 12 or 13 years. Double the time in one place, halve the number of house sales. It wouldn’t be a surprise that more felt it was difficult to move. Low inventory means low supply; so, if everything else stays the same prices will rise. Multiple buyers can find themselves competing which is frustrating, and drives the prices higher. The same number of realtors are trying to earn a living from fewer sales.

A common response is to build more houses. That makes sense, doesn’t it? Building more houses makes sense – as long as it is one house per household. There’s nothing illegal about celebrating career success and frugal money management by buying a second house; but the consequence is that buyers lose an opportunity. A first-time home buyer may have saved up for a mortgage, but in a competitive market their offer may lose out to a cash offer from the buyer who wants a vacation house, or two, or three. Nothing illegal about that. Building more houses is popular though because it means jobs for builders, regardless of who those houses are being built for.

Building more houses isn’t simple, either. Not-In-My-Back-Yard, zoning restrictions, resource limitations, and time complicate and delay the process.

One of my more Frequently Asked Questions is roughly; “Where can I find a fixer-upper, or maybe some land where I can park or build a tiny house?” That fixer may not nice enough for a lender, but is fine for a cash buyer. As for tiny, or even small, or maybe manufactured houses – they may be fine for that person, but the municipality, or the homeowners’ association may say no. The person who wants a house and is willing to compromise is blocked by policies that frequently reach back 50 years to a different world.

Got lumber? It’s expensive, at least for now. Steel stud houses exist, but they aren’t common. Are there enough contractors who know how to build them? Even conventional houses can be delayed because conventional contractors are also in short supply.

Lets go back to that idea of moving. It was easier to “Go west, young man.” But we’ve gone west and are now bouncing around inside settled borders; and ‘young man’ has expanded beyond ‘man’ and ‘young’. West was affordable. Now, west is expensive. People in ‘more affordable regions’ may be able to find opportunities somewhere else, but they may not be able to move there. They are effectively trapped, having to wait for jobs to come to them.

Affordability is an interesting term. Housing is affordable. When every house is selling then someone, or some company, can afford it. A million dollar house is affordable, at least for a while, to whoever bought it. But. Affordability typically refers to the perspective of people who can’t afford a house. The solution is commonly to build more houses that are affordable because, as mentioned before, building is popular (when possible.) To me, solving that affordability has less to do with real estate and more to do with economics. We cheer wages when they increase 5%, but if real estate prices rise 6%, then real estate becomes less affordable for those people. Here comes a copy&paste from earlier. “In the previous year, real estate prices where I live (Whidbey Island) have risen about 15% to 19% depending on the part of the island.” That’s a problem, and it isn’t just a Whidbey Island issue.

Hmm. If the people who want to move to better opportunities could become the contractors building the homes, but they’d need to be able to move here, but they can’t afford that, and … So the situation sits.

Real estate markets are confused. While prices are rising, inventories are falling. It is a seller’s market. It has happened before, but this time the buyers are changing. Corporations and investors are about 18% of the market. Some are buying to rent, diminishing the number of homeowners and raising the number of renters. That also means more people who don’t get the benefit of building equity, instead paying more out for the expense called rent. A bigger concern can be the number of houses that are treated as assets, commodities. Many stocks don’t return 15% to 19%. A stock can become worthless but land almost always has some value. Renting produces income, but renters are a risk that something might go wrong. Even if it is typical wear and usage, an investor has to manage the property or hire someone to do so. Some let it sit and wait for a good time to sell. Those houses are no longer available. A house built for ‘affordable housing’ can be pristine and taken out of consideration while a corporation waits for the proper appreciation.

As a stock investor, the author of a book about personal finance (Dream. Invest. Live., the basis for this blog), and a realtor I may look at the real estate industry differently. I’ve only been a broker for a few years, not a few decades as some of my experienced co-workers. Before then I wrote about real estate for Curbed.com. I watched the rise of Zillow, Redfin, Estately, etc.; and it became apparent that they were probably going to do to real estate what Expedia did to travel. Travel was much more of a commodity because there is little variation in airplane seats, so it was possible to mechanize the process of buying tickets. Houses don’t work that way, except for where they do at least somewhat. Condos and developments are easier to see that way. If the approach works well enough there, would it also work in older, less regimented neighborhoods? How about rural spaces? These corporations act more quickly than the industry. They are willing to try ideas and see if they succeed or fail. That is the disruptive nature of capitalism. No judgment, here.

No judgment, but definitely conversations, especially among the other brokers who got their license about the same time as me. I recall one conversation where three of us agreed that the industry would probably radically change within the next 4-5 years; and of course I mention it because that conversation was about 3-4 years ago. There have been changes, and they aren’t done, yet.

Last year I did a quick analysis and found that in my area about 1/3 of the transactions included discount brokerages. To brokers that means reduced commissions and reduced opportunities in existing careers. Within the last month a senior and experienced broker pointed out that 3/4 of the listings were from outside the area. We are close to Seattle which has many more brokers. They are in a similar situation, so if even a few of them extend their range our way our market drastically shifts, especially when inventories are so low.

People hear about how hot and busy the real estate market is. It is easy to understand why it seems like everyone is making money. But, if there are 12 offers on a house that is good news for the seller and their broker, the winning buyer and their broker (assuming the deal closes), and 11 pairs of buyers and brokers who spent a lot of time and money moving on to the next offering. That’s 12 offers here on an island. I talked to one broker in Seattle who has been involved in listings with over 70 offers. That is a sale, but I also see about 70 frustrated sellers and brokers. Imagine the buyers’ frustrations and understand why they’re willing to bid higher next time.

As I frequently add to social media posts (but not to Twitter because this takes too many characters);

Interesting times for #realestate sellers, buyers, and brokers

(Disclosure: I’m a broker at Dalton Realty, Inc. http://whidbeyrealtor.com/).

(By the way, that disclosure is required, but it is also an example of why real estate communications can seem stilted and stiff.)

‘Interesting times’ is a massive understatement.

I am also convinced that these times are not the New Normal, though they are leading to it. Within the world of finance and economics money flows from assets to assets, regardless of their target’s necessity. Money has been flowing into real estate. Money attracts innovation and challengers. Long-established industries can change when innovation succeeds. Eventually, at least some of the speculative money will move on to the next commodity. Real estate will adjust again, but it will be changed; especially in commoditized markets. The old industry Normal may not be sustainable in such a situation; except possibly in custom and niche markets. Vacation rentals, vacant speculative homes, and a backlog of housing demand will be affecting the New Normal. None of those trends and goals, however, are likely to provide sufficient housing for those who can’t afford it until economies change and personal finances improve to where housing becomes affordable for more, many more.

Discount brokerages are not new. Travel agencies acting as brokerages changed, or vanished. Stock brokerages changed, with some becoming more exclusive and some becoming so affordable that commissions are barely noticeable. The change in real estate brokerages has begun, which might bifurcate into housing that can be commoditized more readily (condos, etc.) and more exclusive (custom houses and rural areas.)

This is happening as inflation rises, a pandemic sweeps through, refugees from disasters struggle to find any kind of place to live.

I don’t have answers (except in my dreams), but at least I can try to answer questions about my area – which I just realized I can use a plug for my talk at Langley Library on May 17 at 6:30PM. It may not be live-streamed (I don’t know, yet), but I hope to record it and post it to YouTube.

As I mentioned above, interesting times.