The world of finance confuses many. The world of economics confuses many. A complete understanding of either is impossible because both are chaotic enough that at some point chance has an effect. To me, the essence of both are four familiar terms: assets, liabilities, income, and expense. Personally, I am very aware of my income and expenses, which is the nature of being an entrepreneur by necessity. Globally, I am watching assets, where they’re flowing, where they’re stuck, and what that’s possibly doing to the economy, my portfolio, and changes in society. These are interesting times.

Personal assets are usually easy to understand: maybe a house, a car, other possessions, some investments, and cash. The flow between them is simple enough. Cash is used for most of them, and debt (liabilities) is used for for a few of them. (Cheer the person who bought their house for cash.)

Assets for corporations, institutions, and the wealthy are harder to understand. The value of the assets is much greater. The leverage is therefore higher; and therefore the incentive to find the best distribution is also greater. Making an extra 0.2% on a personal savings account doesn’t greatly affect someone with a $1,000 account, but 0.2% of $1,000,000,000 is a useful number (especially if that’s the difference between your company paying or not paying you a salary.)

I’ve been listening to the consternations of the 0.1%. They are telling an interesting story.

At the most recent MicroVision stockholders(‘) meeting, the Chairman of the Board repeated something a message I’ve seen in other channels.

“The big money doesn’t know where to put its money.” (Paraphrased because no recording devices were allowed.)

The implications for small corporations like MicroVision is that potential investors are lacking confidence, and are less likely to invest. According to him, tech company IPOs have dropped dramatically. For months there have been reports of a private capital bubble. Small tech firms were receiving large valuations by institutional and accredited investors; just like before the Internet Bubble. This time, however, it didn’t make as much news because retail investors weren’t part of the party. Instead of making money through a public IPO, companies were waiting for private buyouts. The public stock market had gone private, at least to some extent.

Stocks are only one major asset class. Others are commodities, bonds, real estate, and precious metals. Each is having upsets.

Commodities were hit by two main influences. The oil price war dropped prices enough to destabilize governments and implode portfolios. The war was fueled by fracking, which encouraged some consumers to switch to renewable energy, which raised production volume, which when coupled with technological improvements dropped the price of renewable energy enough to encourage more consumers to switch. Now, solar is cheaper than fossil fuels in some places. As electric cars become more attractive, yet more demand drops. The demand drop happening during a supply glut means depressed prices (despite a rebound). Unstable countries have to sell even more to run their governments, further limiting the potential oil price recovery. The other main influence was China’s slowdown. As they reduced their demand for fossil fuels and other raw materials, the world’s mining and refining operations had to scale back, further reducing revenues. Oil and coal, and the other commodities look like risky investments.

Bonds and other lending options are in a weird position. While some destabilized countries are experiencing hyper-inflation (Venezuela is estimated to hit 720% this year), many of the more stable countries are worried about deflation. Too much money is being saved rather than spent. Without money flowing, businesses can’t grow, hire, or enable other businesses. One solution is to drop interest rates below zero. They try to scare the money out of its resting places in banks by paying back less than was deposited. As weird as that is, it hasn’t been enough to move the money. Another sign that financiers are afraid.

Real estate has been visibly weirder. Large parts of the US have barely recovered from the Great Recession (the Second Great Depression) of 2008. Eight years of patience has yet to bring many households back to positive equity. People feel trapped in their houses, neighborhoods, and jobs; and are unable to move to better situations. At the same time, many of the houses that were sold or foreclosed in distress were bought by firms that turned them into rentals. Rents are rising to the point that no state in the US has a median rent that can be met by a full-time minimum wage worker. At the same time yet again, some real estate markets are in hyper-acceleration. Prominent cities like London, New York, and San Francisco have housing markets defined by large cash purchases. If that was because of accelerating economies and the increased workforce that would be appropriate, but in many cases the money is coming in to buy houses and leave them empty. People are buying real estate because it is tangible, it is an easy way to park large sums of money, and things like renters are nuisances that can be ignored. The liquidity of the houses hasn’t been tested, yet. If there’s a crash, the prices may drop enough to let the original buyers back in; but in the meantime the local economies are struggling because the local employees can’t afford the neighborhoods and the neighborhoods have fewer neighbors to support the businesses. Businesses and employees can’t wait forever.

Precious metals have always been a hedge, a safe zone. Over the last few months, gold has begun to recover. It hit a peak in 2011, dropped as the stock markets recovered, and has begun climbing again as the markets have stalled. Even here, though, there has been a hesitancy because of exploitation of people in conflict zones. With everything else going on, that hesitancy may not be significant.

As if it wasn’t bad enough for the 0.1% (cue the very tiny violin), the Panama Papers proved that secrets about tax havens are only as secure as the emotions of the employees. One person proved that 2.6TB of data can walk out the door and into the world. A $300 drive can capture that and more, and fit in your pocket or purse. The Panama Papers have already affected governments and politicians, and that was a small leak that was mostly about people outside the US. A scandal for them, but less important to most Americans. The money hidden in havens managed in Delaware, Wyoming, and Nevada are equally vulnerable, and more likely to reveal Americans who are hiding money from America.

If you’re managing those kinds of finances, moving the money doesn’t look good, and neither does letting it sit somewhere. There are some radical notions, like acting like a business and accepting the risk of investing it, acting like a citizen of some country and paying the taxes, acting like the head of a corporation and properly paying the employees; but, none of those options are evidently attractive. All the more reason to buy another company, sports team, mega-yacht, or more influence.

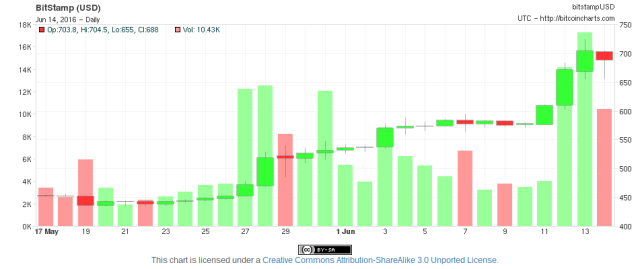

One measure I’ve been tracking is Bitcoin (and other cryptocurrencies.) Within the last year, major financial institutions and some governments have been experimenting with Bitcoin, et al, and its Blockchain technology. There are some attractive aspects for their businesses; but the aspect I’ve been curious about is whether wealth will consider the privacy and increasing legitimacy of digital currency to be a new place to park wealth. Within the last month, Bitcoin has risen from ~$450 to ~$700. That’s an attractive return. Bitcoing has always been volatile, but it is also new. Growing up is a bumpy process. It may be attracting suitors who realize it isn’t just kid stuff.

If none of the other assets change, and Bitcoin, et al, continues to rise, it may be a sign of desparation or legitimacy or both. In either case, that suggests a significant shift in the basic nature of investing and our economy.

In this election year, there’s increased political incentive for someone who opposes a candidate to reveal the reality behind some candidate’s wealth or lack of it. If that happens before November, the repercussions will affect US politics, the US economy, and the rest of the world. As if the world wasn’t uncertain enough, what would happen then? I don’t know (though I have a long list of guesses). I suspect there will be shift in my personal finances; but it will be far less dramatic that the shift some billionaires, corporations, and governments will have to negotiate. Interesting times, in deed.

Obviously I need to read your “Dream. Invest. Live” You totally lose me. But I admire your intelligence and expertise in this field.