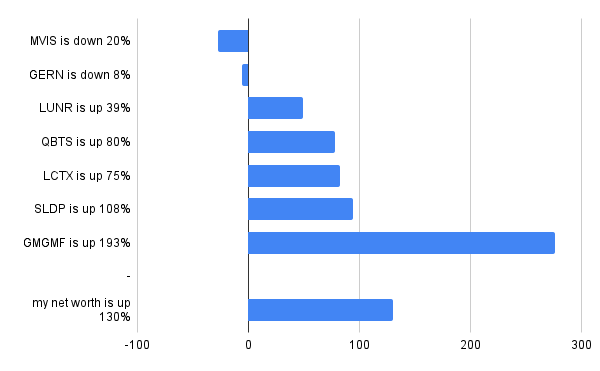

Let’s see. The simplest review is: in the most recent six months:

GERN is down 6%

LCTX is up 83%

MVIS is down 27%

GMGMF is up 276%

SLDP is up 94%

QBTS is up 78%

LUNR is up 49%

and my net worth is up 130%, and that’s after expenses and taxes and such.

Not going to complain.

Going to keep worrying.

There are good reasons for the growth in these companies, particularly in quantum computing (QBTS), lunar industry development (LUNR), and solid-state batteries (GMGMF and SLDP). Biotechs are as squirrely as ever (GERN and LCTX). MVIS is as encouraging and disappointing as ever.

In terms of personal finances, life is good. My house price hasn’t changed much since I bought and moved into a tiny house. Evidently, even though I am feeling spendy, I continue to live reasonably frugally, though now that is by choice instead of necessity. My income is dominated by Social Security because it has been over a year since I’ve had a job. I continue to write and produce books and photos, but they’re sales have been slow, possibly as I rush-wrote my book about my roller-coaster ride through America’s wealth classes, Muddling By. While I watch my stocks every day, I think I only made one sale this year, of which a big chunk was re-invested, a chunk went to paying off personal and emotional debts and thanks, and the rest resides as a cash buffer to ease money anxieties.

So, that was 2025.

I’m staring at 2026. I think change is accelerating, as is to be expected in a singularity, that the changes will mostly be unsurprising, and that a few changes will surprise almost everyone. Someone will get lucky and guess right, but they’ll probably claim it as foresight. Singularities are unpredictable, almost by definition.

I’m staring at 2026 because I: 1) know that most days are like the previous days, and 2) change is changing and fundamental assumptions may prove to be good ideas but not natural laws.

Aside from aliens and such, AI can be the biggest swinger in the world order. Climate change is happening. Politics is eating itself. Injustices are harder to hide, yet remain too-intractable. We are an immature species pretending that we know what we’re doing. We’re smarter than before, but a few generations from now we will be seen as silly and stupid.

So, in terms of personal finance, I’m trying to decide on what I should do with what I have.

Money is one issue because the investment community has been changing for decades, computers accelerated those changes, and AI may overwhelm any of those trends. AI may invest, but even if it doesn’t industries will be challenged, which means stocks will be challenged, which means I shouldn’t expect things to stay the same.

I’ve been investing since 1977 and have seen several bubbles, corrections, and recoveries. I started this post with some impressive numbers, of which I am glad, but those numbers are large enough that it seems like yet another bubble. And yet, crashes have not been complete, some stocks go up as others go down, fear is the enemy but prudence suggests being ready to move based on reality.

I think AI may pop, which is one reason to not be invested in it, and yet, quantum computing may survive and thrive because: 1) it may be the next evolutionary step in our technological society, and 2) quantum computing may may may produce or provide a more energy and resource efficient infrastructure for many technology requirements and advances.

I wrote Firewatcher, a sci-fi novel about people escaping Earth to escape an AI, partly because I heard projections of AI advancements happening in 2100, if ever, and produced my estimate of 2040. As I started writing the book in the 2010s, I realized that AI was maturing faster than that. I’m glad I finished it in time. 2030 wouldn’t be a surprise to me, and neither would ‘any day now’.

At least for now, I will continue to be mostly invested in the stock market because:1) if I’m wrong, stocks will still be investments, 2) I think my stocks are well-positioned for such change, and 3) I’m not so worried that I’m going to go all prepper and head out to the hills (which are right up the road, but I don’t have enough cash to buy a good piece of land with a house, and have comfortable income too.)

And, I consider climate change, regime change, societal change, and whatever change because those changes aren’t going to stop while AI blows by or blows up. I think AI could solve those issues, but I think we’ll go through a period of it and us confusing us. We may be years from resolving most of those issues, and the world may require years for the global changes.

Whew. So much for this post just being about my investments and personal finance. And yet, of all the years that I’ve done this twice-yearly exercise, now seems to be closest to the beginning of a crucial era in our civilization’s development.

I suspect 2026 will be a news-heavy year, a time of significant changes, and a time to be glad of the frugal, practical, creative, and pragmatic people I know because they may be the examples that people scoff at now and soon find they have to listen to intently.

Wish us all good luck for the new year, and if it is a happy one that will be a bonus.

And, I still buy lottery tickets.

Read on for my stock synopses. And good luck.

INTRO Here’s my semi-annual exercise to see if I remember why I own the stocks I own, and so I can check back and see if their stories have changed. I post in case it helps others too.

(I’ve also collected links to the other discussion boards and my other stocks over on my blog. https://trimbathcreative.net/ & from my One Company One Story series on YouTube https://youtu.be/su1AMjPEkLI )

Geron

GERN (market cap is $0.855B was $0.870B)

Geron (GERN) is a biotech that recently received FDA approval for their blood disorder treatment. Their product works on blood-related cancers, and may extend to other cancers.

Geron is a biotech, but seems a bit withered. I’ve held the stock since circa 1999. Then, they were leading edge, a major innovator, had grand plans for dramatically expanding human lifespans; and had a management team and philosophy that impressed me with their wisdom and insights into public reactions.

Delays inspired and required the sale of much of their intellectual property and divisions, which leaves them with the telomerase-related treatments. They may be more than good enough for the company to become impressively useful and profitable. Sadly, subsequent management teams seem to have lost the startup vigor, and the long term grand plan for revolutionizing medical care. Now, management seems like, well, managers, managers who are executing a plan but not a vision.

As I understand it, managing cell telomeres can manage to treat cell death by encouraging some cells to die (cancer) and discouraging others from dying prematurely (auto-immune diseases). Those two general applications cover a broad swath of medical issues, some of which have few or poor treatment options. Whether management recognizes the potential is highly uncertain.

DISCLOSURE LTBH since 1999 and continuing to hold, but do not plan on buying more unless I see significant positive changes at the company. I continue to hold because selling so low has little benefit and I am an optimist.

Graphene Manufacturing Group

GMGMF (market cap is $0.239B was $0.064B)

Graphene Manufacturing Group (GMGMF) is a startup with a few released and potential products based on the use of graphene. My primary interest is in their battery work, but they also sell lubrication and cooling additives.

I suspect we are about to reach the next plateau in battery development. Particularly, GMGMF recently announced a solid state battery that will recharge in 6 minutes. Insert exclamation mark. (!) I recall whatever came before alkaline, then rechargeables, now, lithium-ion. Graphene allows batteries that are safer, thinner, and recharge quicker. Such advantages could lead to greater adoption of electric vehicles and other devices, both large markets.

I am a fan of graphene, and believe a next generation battery is due. Whether it is GMGMF or someone else will be determined by market conditions. Unfortunately, I can’t invest in all of those publicly-traded companies, so I picked two: GMGMF and SLDP. Both may be years away from profitability, though the stocks may move in anticipation instead of reaction to news.

DISCLOSURE I tend to LTBH, and have held shares since 2024.

Lineage Cell Therapeutics

LCTX (market cap is $0.368B was $0.210B)

Lineage Cell Therapeutics (LCTX) is a startup biotech diversified across several technologies, though I follow them, and own stock, because of their work in using stem cells to treat nerve damage and vision-related maladies (macular degeneration).

Stem cell-based treatments are innovative enough that the FDA approval process can become more difficult. The treatments may not have current approved competition that could guide the FDA, and trial sizes tend to be smaller. Conventional approaches may have much larger groups, and therefore, larger and statistically more significant results. The fewer the folks, the greater likelihood of a result being seen as a fluke rather than a result. LCTX’s treatments are further from approval than I expected. Compassionate care would suggest their use when no other treatment is available.

Their early results are encouraging, and similar to what they said they expected to achieve. Vision improvements rely on data because they are harder to verify than the objectively visible improvement of turning a quadriplegic to a paraplegic.

Approval is likely a few years away, but they’ve been working on the treatments for years, so it may not take much more time, relatively.

DISCLOSURE LTBH by habit, but having to remember that my LCTX/BTX holdings came from AST (2014), which was spun off from GERN (which I’ve held since 1999). I hear patience pays, but it is easy to have doubts after twenty years of waiting.

Intuitive Machines

LUNR (market cap is $2.87B was $1.94B)

Intuitive Machines (with the more appropriately named symbol LUNR) is an aerospace company largely focused on delivering aerospace products and services into the lunar industry, economy, and exploration. Recent acquisitions may diversify them into more general space-related endeavors. They are a relatively young company in a relatively young industry.

LUNR is probably mostly known for having both lunar landers land on the moon (good) then fall over (bad). While those are publicly perceived failures, the stock seems buoyed by the fact that the company met 85% of the mission goals, and were paid for them.

They are not alone. Many companies are addressing the lunar market and having varied successes. Anything involving rockets is risky. Going farther than low-earth orbit is rare and relatively unexplored territory, but the potential demand and market is enormous – and largely ill-defined. The discovery of lunar water has been a great enabler that wasn’t as important in the Apollo era.

LUNR’s diversification is a plus. LUNR’s overlooked successes, regardless of tipped landers, may suggest an undervaluation. Rockets also involve governments, and industrial risks. Such worries can constrain the stock.

The lunar market could be our species’ first extra-planetary industry and economy, in which case, this could be a ground-floor opportunity (for a redefinition of ‘ground’).

If the next lander lands successfully, the company may gain a significant legitimacy, and commensurate stock price. If. If. If.

DISCLOSURE LTBH since 2024. Bought more, recently.

MicroVision

MVIS (market cap is $0.259B was $0.283B)

Oh dear. Am I doing this again? Is the company doing this again, a new CEO which means yet again a new direction? Sigh. Read on, and hope. For years, I’ve copied and pasted the previous post. Let’s start fresh.

Microvision (MVIS) is a (perpetual) startup based on the technology that is an oscillating mirror on a chip. Shine light on the mirror and the oscillations can produce an image. Let the mirror reflect what it sees, and it becomes a sensor. Shine light on it and receive that reflected light, and it is effectively LiDAR. The market potential for the projector is roughly the same as the smartphone market because a projector has already been produced that fits in a smartphone. As a bar code sensor, it has been demonstrated for reading barcodes as well as helping industrial automation. As a LiDAR unit, it can enable autonomous vehicles. Lots of potential.

Lots of potential, but each CEO has departed without their initiative becoming successful. Arguably, some of those ideas may have and could be profitable, but they were set aside as new managers arrived. This has been going on since at least 1999. The company has survived through dilution, which means my original stake has been diminished significantly. I believe in the potential based on market needs, not personal emotions. I am also saddened by the correlation of shifting development directions with each new management shift. The ideas that have been abandoned have rarely been explained in terms of market conditions and are replaced with the prospects of the next shiny option, and yet, I suspect some of those earlier ideas may be valid if they’d pursued them or returned to them.

DISCLOSURE LTBH since 1999 (though the very first shares are gone). I continue to hold because the price is so low that the only benefit to a sale may be for tax losses, and because, if only by luck, I think the company may be profitable because a customer wants the product regardless of what management has in mind.

Dilution means that I no longer have more than enough if the company finally succeeds and the stock reaches the heights I think are possible. Some day, some day…

D-Wave Quantum

QBTS (market cap is $9.19B was $4.56B)

D-Wave Quantum (which has the much cooler symbol QBTS) is a leading edge quantum computer company that is delivering products and services to an industry that is a large unknown with large potential. Quantum Computing can also be 1) relatively easy to describe as a computer with bits that are 1s and 0s, and 2) can be ridiculously difficult to explain in terms of operations.

Quantum computing had been a lab tech possibility for so long that I think QBTS and others were overlooked. Now, the market is realizing they are real, and the market is confused, excited, and worried about how to value the technology and the individual players. As the actual computers find uses, there is an additional difficulty in understanding the nuances that delineate and define a variety of hardware and software approaches.

Within the recent 18 months, the stock has risen from ~$1 to ~$46 and settled back to ~$30. Optimists can say it is up 2,000%. Pessimists can say it is down 33%. Both are right. What happens next is a gamble. I doubt there were many investors who recognized how large Intel, et al could become. Now that we’re seen the phenomenal growth in new technology, the rush is on to not miss out on quantum computing, just in case. That also means the stock price is driven by hope more than fundamentals, at least for now.

QBTS is not alone, however. Their early success is more than encouraging, but innovative technologies are known for disruptions from unexpected innovations – or maybe QBTS is the unexpected and therefore profitable innovation.

DISCLOSURE LTBH since 2024. Sold some shares to cover my investment. Sold some shares to realize a profit. Holding the rest because 1) they’re all profit, and 2) if QBTS succeeds as much as it could, these shares could look cheap, maybe.

Solid Power

SLDP (market cap is $0.817B was $0.398B)

Solid Power (SLDP) is a startup working on solid-state batteries.

I suspect we are about to reach the next plateau in battery development. I recall whatever came before alkaline, then rechargeables, now, lithium-ion. Graphene allows batteries that are safer, thinner, and recharge quicker. Such advantages could lead to greater adoption of electric vehicles and other devices, both large markets.

Solid state batteries are, ideally, safer than lithium-ion. That alone is sufficient to encourage their adoption, and if they charge faster or have greater density, the adoption and profitability can increase.

I believe a next generation battery is due. Whether it is SLDP or someone else will be determined by market conditions. Unfortunately, I can’t invest in all of those publicly-traded companies, so I picked two: GMGMF and SLDP. Both may be years away from profitability, though the stocks may move in anticipation instead of reaction.

DISCLOSURE LTBH since 2024.

For more details about the stocks, here are links to various discussion boards where you can find my synopses, as well as others’ points of view. For more details about how I do what I do, there’s a book that I wrote at the request of several friends: Dream. Invest. Live. Maybe you can help my personal finances by buying a copy – though the frugal part of me recommends checking one out from a library.

Many of the independent investors who contribute to the discussions provide in-depth analyses that either aren’t available elsewhere, or would cost too much to buy. The other advantage is the diversity of perspectives. Unfortunately, I don’t engage as much as I did before. Some discussions have degraded due to lack of moderators, or overly zealous moderators (immoderate moderators, an oxymoron), or have too many immoderate voices. Some boards are effectively ghost towns, or feel like cavernous empty warehouses.

“Gold mines produce far more rubble than gold.

It is easy to complain about the rubble.

Ignore the rubble.

Pay attention to the gold.”

Regardless, here are the sites I continue to visit, even if it is only to lurk and listen.

I encourage you to tune in, because more voices (as long as they’re mature) make for a better conversation. Maybe I’ll read you there.

Investor Village (widest range of boards, could benefit from more traffic)

Silicon Investor (Relatively older boards, less trafficked, but populated with informed investors)

Reddit (Many will cringe, but there’s impressive quality within the impressive quantity of posts and voices. I lurk more than post.)

Intuitive Machines (LUNR)